.

.

According to Caprio and Levine (2002), corporate governance in the banking industry meets two essentials problems: (i) agency problems in banking industry is in very high levels (ii) regulation and supervision that are applied to the banking industry, in a separate level, even can off-set the mechanism of the corporate governance itself. Hart (1995) stated that the corporate Governance arises when the agency problems in internal corporation increase and the transaction cost can not be solved by a contract explicitely. The statement is supported by Fama and Jensen (1983):

“…agency problems arise because contracts are not costlessly written and enforced”Agency problem in the banking industry has the different dimension with the other industries since there is a regulator’s role which represents stakeholders’ needs. Related with the state-owned bank, agency problems are getting complex since the possibility of the rising of multi agents and principal (Tandelilin, 2004). So that, in the banking industry there is a dimension of principal- agent problems that are different with another industry (Llewellyn and Sinha, 2000).

Agency problems in the banking sector are in two categories. The first is the agency problem caused by debt (agency cost of debt) and the second is the agency problem that related to the separation of ownership and control. Ciancanelli and Gonzalez (2000) stated that the approach the agency theory which are trusted to be existed in order to understand the corporate governance problems in the banking industry has to be reevaluated because of the difference of the basic premise of the agency theory used and the characteristics of the banking industry in spite of the problem of the asymmetrical information that is related to all of the sides.

The corporate governance in banking industry is related to two things. First, the external corporate governance with its financial safety nets and prudential regulation. Second, internal corporate governance with its accountability, disclosure, and transparency that departs from creating the arising of the bank system and minimizes the moral attitudes deviation. By using the frame of the corporate governance in banking industry by Ciancanelli (2000), Nam (2004), and Mehran (2003), this research develops three construction : (1) External corporate Governance (ECG) (2) Internal Corporate Governance (ICG) and (3) Type of Ownership.

THEORITICAL FRAMEWORK

Corporate Governance includes (1) set of rules that sets the relationship of the shareeholders, manager, creditor and others deal with the rights and responsibility of each side, and (2) set of mechanism which guarantees direct and indirectly of the application of the set of rules (ADB, 2001). Deal with the banking industry, OECD (1999) described corporate Governance as follows:

……’a set of relationship between the company’s management, its board, its shareholders and other stakeholders. Corporate Governance also provides the structure through which the objectives of the company are set, and the means of attaining those objectives and monitoring are determined. Good corporate governance should provide proper incentives for the board and management to pursue objectives that are interests of the company and shareholders and should facilitate affective monitoring, thereby encouraging firms to se the resource more efficiently’Macey and O’Hara (2001) stated that corporate governance in banking industry has a wide thought since there is a type of specific contractual that happened in the banking industry, some of them are the protection to the shareholders and stakeholders. Besides that, the specific characteristic of bank needs government’s intervention in the type of regulations and supervisions to control the bank management’s act.

External Corporate Governance

It is clear that developing models of corporate governance in banking requires that we understand how regulation affects the principal’s delegation of decision making authority (Jensen and Smith, 1984) and what effects this has on the behaviour of their delegated agents. (Freixas and Rochet, 1997). Regulation has at least four effects. Firstly, the existence of regulation implies the existence of an external force, independent of the market, which affects both the owner and the manager.

Secondly, because the market, in which banking firms act is regulated, one can argue that the regulations aimed at the market implicitly create an external governance force on the firm. Thirdly, the existence of both the regulator and regulations implies the market forces will discipline both managers and owners in a different way than that in unregulated firms. Fourth, in order to prevent systemic risk, such as lender of last resort, the current banking regulation means that a second and external party is sharing the banks’ risk. (Ciancanelli, 2000).

As the external corporate governance mechanism, banking regulation reflect in safety nets facilities such as deposit insurance (explicit and implicit) and lender of the last resort of central bank. In order to keep financial safety nets from moral hazard, generally, the government applied the prudential regulation and supervision. In this case, Dewatripoint and Tirole (1993) stated that the prudential regulation and supervision mostly meant to keep the bank solvency and as the incentive for stakeholders to control or apply the corporate governance in banking sector widely.

Internal Corporate Governance

The Bassel Committee on banking supervision (1999) stressed that the board and senior management are in fully responsible in apllying good corporate governance. In order to support the effectiveness of editorial board’s work, some aspects are needed to consider about, they are: board’s structure and independency, function and activity, compensation and other obligations (Nam, 2004). The internal corporate government in this research is divided into two; they are internal corporate governance- manager (ICG- manager) and internal corporate governance owner (ICG- owner). The difference of ICG- manager and ICG- owner is in the focus control. ICG- manager stressed to the internal of the manager which is stimulated externally through the attention of the owner to the manager’s interest which is actualized in the remuneration and the other types of another human resource development to increase the bank revenue (Jensen and Murphy, 1990). The ICG- owner stressed in the control throughout the manager to increase the efficiency.

Ownership Dispersion

Ownership dispersion depends on the numbers of shareholders. Practically, the extreme focused types of ownership are often faced in the close private bank. However, the dispersed type of ownership is state-owned bank, because the government act as an agent. Between the both of those extreme points, there is a possibility to the private bank to sell some of their stakes to the public. So that creates the form of majority and minority ownership. Husnan (2001) explained the agency problems to the ownership dispersion in the frame of corporate governance by grouping the company based on the three characteristics of the ownership. The three of the characteristics are (a) dispersed ownership (b) closely held ownership and (c) the state owned firms.

Theoretical background

Conceptually, this research classified the type of the bank ownership into four groups. They are:

- Foreign or joint venture bank

- Private unlisted bank

- Private listed bank

- Government (state-owned) bank

This structure of ownership is an extreme closely held ownership, because the relatively small amount of the owner are able to fully control management mechanism for maximizing the company’s financial performance. As the result, the degree of the agency problems between the owners with the manager tend to be low.

The public private bank moved the degree of the agency problems in Indonesia to conflict of the major owner’s interest and the minor one. Agency problem might be different if there was no major owner who controlled the management. The wide dispersed ownership by the public will move the agency problems to the conflict of interest between the dispersed owners with the manager. The condition in Indonesia indicated more in the major owner who controlled the management’s performance, so it’s potential in raising the conflict of the majority and the minority. The state-owned bank is a unique ownership because practically, there is no pure owner who can control to the company management. The government, both in context of the executive and legislative and all sides related with the management of the state-owned bank as an agent without principal. However, the state-owned bank is a chosen ownership that extremely against the closely held ownership, because the forms of the ownership are dispersed completely. So, the degree of the agency problem in this are is counted as the strongest relatively compared with the other forms of ownership.

Based on the typology of the ownership’s form and potential agency problems, it is possible to describe the agency problems in banking industry as in table 2-1. In the table, the agency problems might happen between the owner vs. manager and between the manager/ the owner vs. creditor or the minority.

| Type of Conflict | Reputable Foreign Bank | Private Bank | Public listed Bank | State-owned Bank |

|---|---|---|---|---|

| (Proxy for GCG) | Closely held | Minority-majority | Dispersed | |

| Manager vs. owner | > | |||

| Manager/owner vs. Creditor/ Minority |

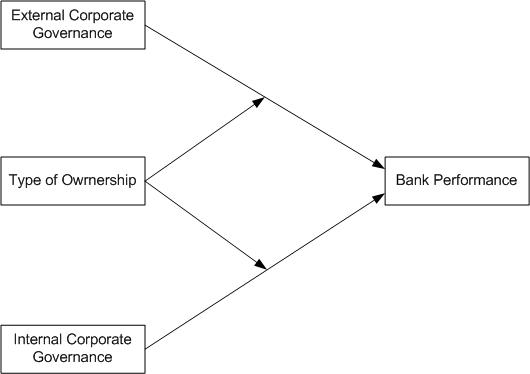

RESEARCH MODEL

The agency problems caused firm performance cannot run optimally. The way to detect the agency problems is learning the management efforts which are related to external corporate governance as well as internal corporate governance. The different type of ownership have the different level of utility and the different ability in controlling the management. Figure 2-1 shows the research’s framework that bank performance is effected by three exogenous constructions.

Research Framework

External Corporate Governance. This research used the aspect of regulation and finance supervision as the reflection of external corporate governance by stressing the in the obedience factor to regulation and supervision. The composite variable of regulation obedience is in the form of logistic probability that is used as proxy of external corporate governance. The higher the probability of the regulation’s obedience and so higher the bank willingness to operate the company under the regulations. The external corporate governance variables that related to the regulation’s obedience consist of capital aspect and earning assets. This research used the government classification about the healthy and unhealthy bank during 1999 until 2001 to build analysis model. There are the evidence for the score: 1 for healthy bank and 0 for unhealthy bank. The unhealthy banks or under controlled banks reflect the consequence of the failed bank management attitudes or disobey the regulations. The healthy banks reflect the discipline of the bank management in obeying the regulations.

Internal Corporate Governance-manager are taken from pay-performance sensitivity. Jensen and Murphy (1990) had a research about pay-performance sensitivity. Pay-performance sensitivity is reflected from the parameter coefficient which is estimated with the pay regression model and the incentive to the wealth of the stakeholders. In this case ICGM is the internal corporate governance as the manager’s interest representation that are taken from the estimation of parameter coefficient.

Internal Corporate Governance-owner. ICG-owner is owner’s direct interference in the form of manager controls. Some of them are in actions on behalf of and for owner and the command for internal editor. The essence of the ICG- owner is in the efficiency factor of preventing manager from doing his own interest. Net interest margin (NIM) represents ICG- owner. This research has an assumption that the use of NIM in a period hasn’t reflected the appropriate mechanism for the owner in applying ICG owner. In other words, this research stresses to the stability of NIM from one to another period that reflected more in the success of the owner control mechanism than in the applying of NIM in a period. So that we use coefficient of variation NIM reflected internal corporate governance-owner interest.

Generally, empirical research of the effect of corporate governance and type of ownership to the bank performance can be explained by agency theory. However, there is a dimension of principal agency problems that are more complex in banking industry that cannot be found in non-financial banking industry. Besides, the existence of regulation factor as the reflection of public interest caused the control market mechanism as one of the mechanism of corporate governance to discipline the manager to become more useless. Moreover, with deposit insurance program, investors tend to be passived in controlling to prevent every risk increasing that are done by the owner or the stakeholder.

The agency theory, formalized by Jensen and Meckling (1976), posits that the agency costs of deviation from value maximization increase as managers’ stakes decrease and ownership becomes more disperse. Agency problem in banking industry in the context of corporate governance through the approach of ownership dispersion results as follow:

- the interference of regulation in the concentrated ownership (private unlisted Bank) and dispersed ownership (state-owned bank) caused agency problems in high level degrees. This result is in line with the view that is based on the ownership’s aspect stated that the state-owned companies naturally are less efficient than the private companies. Governance view stated that private companies are more successful in handling the corporate governance problems than the state-owned companies. Reversely, private ownership are based on their skills that are better in contracting and incentives (Schleifer and Vishny (1994) ;

- Regulation intervention in less concentrated ownership (private listed bank) caused the agency problems fall in lower level degree. According to the agency theory, the separation of ownership and controlling functions between the principal and agents is possible to happen in the private listed bank than in the private unlisted bank. However, in banking industry, the agency problems that raised between the major and minor shareholders or between the manager- stakeholders “are ignored” by the function of regulator (Llewllyn and Sinha, 2000).

Klik tombol like di atas... Jika anda menyukai artikel ini.

Terima Kasih telah mengunjungi Tautan ini,

Jangan lupa untuk memberikan komentar pada form di bawah post ini.

Maturnuwun...

Terima Kasih telah mengunjungi Tautan ini,

Jangan lupa untuk memberikan komentar pada form di bawah post ini.

Maturnuwun...

Tags:

Tags:

Comments :

Views All / Send Comment!

Post a Comment